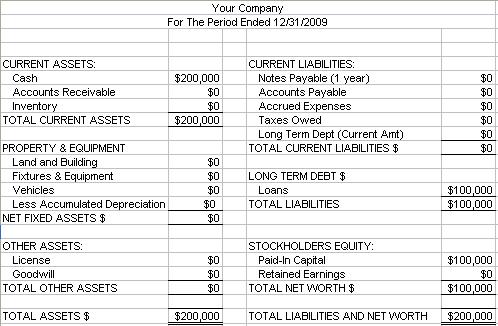

We've previously discussed what Assets are. In an unclassified balance sheet where you only have 3 major classifiations (assets, liabilities and owners equity) that would be in the story. A much more useful report is the Classified Balance Sheet. Here, the three major categories are subdivided to provide readers of the financial statements with much more detailed information. The first such subdivision under assets is Current Assets.

Current Assets are defined as those assets which will either be converted into cash or otherwise 'used up' by the business in a relatively short period of time (generally one year or less). On the balance sheet, they are generally presented in order of liquidity; thus cash is generally listed first.

Other examples of current assets include accounts receivable, notes receivable (which often have a current and a non-current portion) and prepaid expenses. These will be examined in future entries.

Almost as common a term as cash nowadays, accounts receivable is an accounting term meaning amounts owed to a business by other business or customers (individuals or otherwise). An accounts receivable arises anytime when goods are sold but cash is not received immediately; thus when you purchase something for cash at Walmart you are not creating an accounts receivable. If you commit to purchase something (say a lawnmower) and you are offered the option to pay next month, now you have created an accounts receivable on the retailers books.

Almost as common a term as cash nowadays, accounts receivable is an accounting term meaning amounts owed to a business by other business or customers (individuals or otherwise). An accounts receivable arises anytime when goods are sold but cash is not received immediately; thus when you purchase something for cash at Walmart you are not creating an accounts receivable. If you commit to purchase something (say a lawnmower) and you are offered the option to pay next month, now you have created an accounts receivable on the retailers books. Unlike a note receivable (to be discussed next), there is generally no signed agreement beyond an invoice for an accounts receivable. They are generally short term in nature (less than a year, if not only a couple months). Because of their short term nature, they are generally listed as a current asset on the balance sheet next after cash.

Unlike a note receivable (to be discussed next), there is generally no signed agreement beyond an invoice for an accounts receivable. They are generally short term in nature (less than a year, if not only a couple months). Because of their short term nature, they are generally listed as a current asset on the balance sheet next after cash.

include? Cash includes any deposits available in the bank as well as anything on-hand which might include bills and checks or money orders to be deposited.

include? Cash includes any deposits available in the bank as well as anything on-hand which might include bills and checks or money orders to be deposited.